End-of-line automation ROI has become a critical metric for manufacturers operating in highly competitive markets.

It is defined by financial performance.

Return on Investment (ROI) remains one of the most powerful indicators of how effectively a company manages its resources.

ROI is not just an accounting ratio.

It reflects every operational decision made inside the factory.

Capital Expenditure Classifications and Their Role in Maximizing ROI

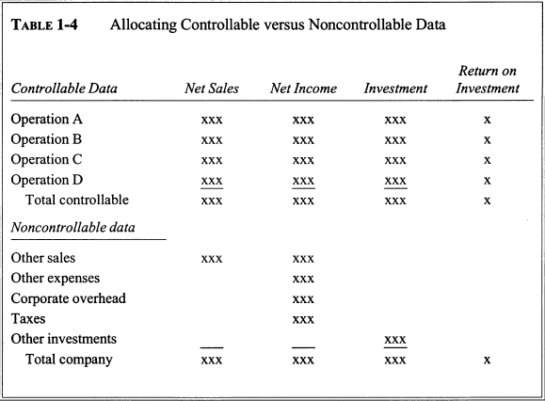

Within any capital expenditure program, investments should not be treated as isolated purchases. Instead, they should be systematically classified into well-defined categories. This structured approach enables organizations to group projects according to strategic priorities and, in turn, establish clear return on investment (ROI) objectives for each major classification.

By organizing capital projects in this way, companies can allocate resources more effectively and ensure that every investment contributes positively to overall financial performance. The objective is not only to maximize ROI within each individual category, but also to optimize returns across the entire organization.

Throughout different stages of a company’s economic life cycle, investment priorities naturally shift. At certain times, the focus may be on cost reduction initiatives. In other periods, emphasis may be placed on modernization, compliance with environmental or safety standards, technological upgrades, capacity increases, new product development, expansion into new markets, or even operational consolidation. Capital resources must be distributed among these varying needs in a balanced and strategic manner to achieve the highest possible return.

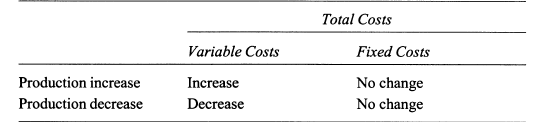

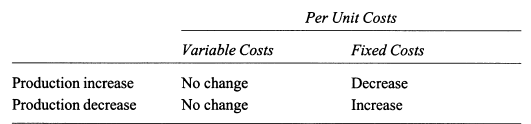

Break-even analysis becomes especially meaningful in automated production environments, where the balance between fixed and variable costs shifts significantly. Automation typically increases fixed costs through investments such as equipment, depreciation, and system integration, while simultaneously reducing variable costs like direct labor, handling, and error-related losses. As production volume increases on an automated line, fixed costs are spread over a larger number of units, causing per-unit fixed costs to decrease, which accelerates the break-even point and improves overall profitability. At the same time, variable costs remain relatively stable on a per-unit basis, since automated processes deliver consistent cycle times and material usage. This dynamic explains why automation favors higher utilization rates: the more an automated system operates, the lower the cost per unit becomes, turning production scale into a key driver of financial performance.

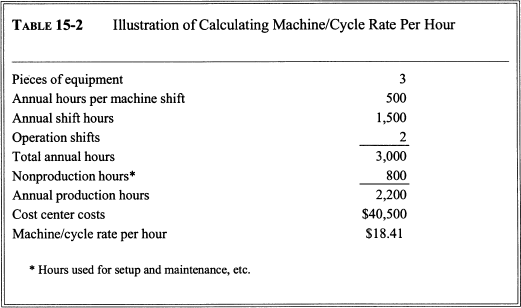

These cost allocation approaches become particularly relevant in automation environments, where precision, cycle time, and equipment utilization directly determine financial performance. In automated production lines, machine hours and cycle time-based costing allow manufacturers to assign costs accurately according to how long each product occupies robotic cells, conveyors, palletizers, or processing units. This makes it possible to measure the true cost impact of slow cycle times, micro-stoppages, or inefficient programming.

Similarly, in integrated automation systems where multiple machines operate as a synchronized unit, line or cell-based costing reflects the reality of modern production flows costs are distributed across the entire automated line based on throughput rather than isolated machines. Finally, in semi-automated environments where human operators support robotic systems, a production manpower pool helps distribute labor costs across multiple automated cells, highlighting how automation can reduce dependency on direct labor while improving cost transparency. When applied correctly, these tools transform automation from a technical upgrade into a measurable financial optimization strategy.

LEASING -AN ALTERNATIVE FINANCING METHOD FOR INCREASING ROI RATES

In automated manufacturing projects, asset acquisition and financing decisions are just as critical as the technical design of the system itself. Investments such as robotic palletizers, conveyors, AGVs, or complete end-of-line lines require significant capital, and the method used to obtain these assets directly influences return on investment. Leasing provides manufacturers with an alternative to large upfront purchases by allowing them to use advanced automation equipment while preserving cash and borrowing capacity for other strategic needs.

By reducing the immediate capital tied up in assets, leasing can improve balance sheet efficiency and free working capital for expansion, inventory, or additional productivity improvements. Depending on whether an operating or capital lease structure is used, the financial impact—assets, depreciation, expenses, and debt—will differ, which ultimately affects reported ROI. For this reason, leasing automation systems can function not only as a financing tool but also as a strategic mechanism to accelerate technology adoption while maintaining stronger financial flexibility and higher overall investment returns.

Understanding the ROI Formula in Manufacturing

At its core:

ROI = Net Income / Investment

But more practically:

ROI is driven by two key components:

- Profitability Rate (Net Income / Sales)

- Turnover Rate (Sales / Assets)

This means: A factory can increase ROI by:

- Increasing profit margins

- Increasing asset utilization

- Or both

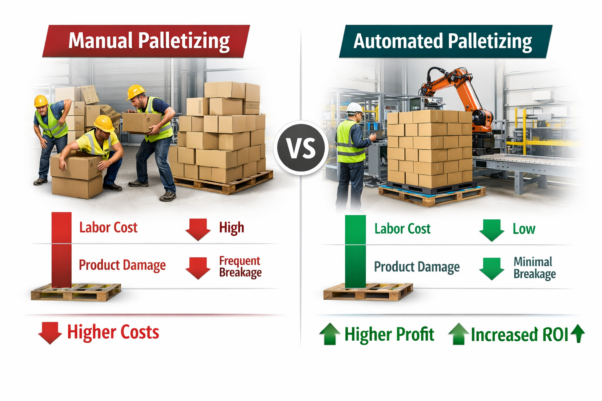

At the end of a production line, the real story of profitability quietly unfolds. A filling machine may run flawlessly upstream, but if cartons are stacked manually, wrapped inconsistently, or damaged during handling, the financial performance of the entire factory begins to erode. This is where end-of-line automation changes the narrative. Instead of multiple operators lifting, aligning, and correcting pallets under time pressure, a robotic palletizing system performs the same task with precision and repeatability. Labor intensity decreases, workplace injuries become far less likely, and stacking patterns remain perfectly consistent shift after shift. Breakage drops, rework is reduced, and downtime caused by human fatigue or inconsistency nearly disappears.

The financial impact is subtle but powerful. Fewer operators are required to supervise a fully automated cell, operational variability declines, and the cost of damaged goods shrinks. What once appeared as “normal production losses” becomes measurable savings. As operating expenses decline, net income increases—strengthening the profitability component of ROI. In this way, end-of-line automation does not merely improve workflow; it reshapes the economics of the line. The transition from manual palletizing to automated palletizing is not just a technological upgrade—it is a direct transformation of operating profit, reflected clearly in the return on investment.

Increasing Turnover Rate (Asset Efficiency)

ROI literature emphasizes that improving asset utilization is just as important as increasing profits

In many factories, the hidden issue is not low margin — it is low asset productivity.

Examples:

- Bottlenecks at palletizing slow down upstream filling lines

- Excess inventory builds due to poor material flow

- Forklift congestion reduces warehouse efficiency

- Working capital increases unnecessarily

End-of-line integration improves:

- Flow synchronization

- Inventory turnover

- Space utilization

- Throughput per square meter

This increases sales supported by the same asset base — improving the turnover rate.

Why the End-of-Line Is the Fastest ROI Zone

the Fastest ROI Zone

Not all automation investments deliver returns at the same speed. Large upstream process machines often require complex redesigns, long commissioning periods, and significant operational disruption before benefits become visible. As a result, payback periods can extend over many years.

End-of-line automation behaves differently.

Because these systems sit at the final stage of production, improvements translate almost immediately into measurable financial results. Labor requirements drop quickly. Handling errors decrease. Damage and rework shrink. Most importantly, bottlenecks disappear, allowing existing upstream equipment to operate at full capacity.

In many cases, companies discover that they do not need additional production lines at all — they simply needed to remove constraints at the end of the line.

This is why end-of-line projects frequently deliver shorter payback periods, often within one to three years. Instead of large structural changes, they unlock value from assets that are already in place. The factory becomes faster without becoming bigger.

From an ROI perspective, few investments offer such direct and rapid impact.

Automation as a Strategic Decision Tool

Ultimately, automation should not be evaluated purely as an engineering upgrade. It is a strategic financial decision.

ROI analysis does not replace managerial judgment, but it provides clarity. It shifts the conversation from intuition to measurable outcomes. Rather than asking whether automation is affordable, leaders begin to evaluate what the current inefficiencies are truly costing the business.

When labor expenses continue to rise, when customer expectations demand shorter lead times, when price pressure reduces margins, and when safety requirements grow stricter, maintaining manual or semi-automated operations carries its own hidden cost.

In this context, automation is no longer optional.

It becomes a necessary step to protect profitability, stabilize operations, and sustain competitiveness.

In other words:

Automation is not an expense.

It is an ROI multiplier.

Conceptual ROI frameworks adapted from:

Rachlin, R. — Return on Investment: Tools and Applications for Decision Making, Routledge